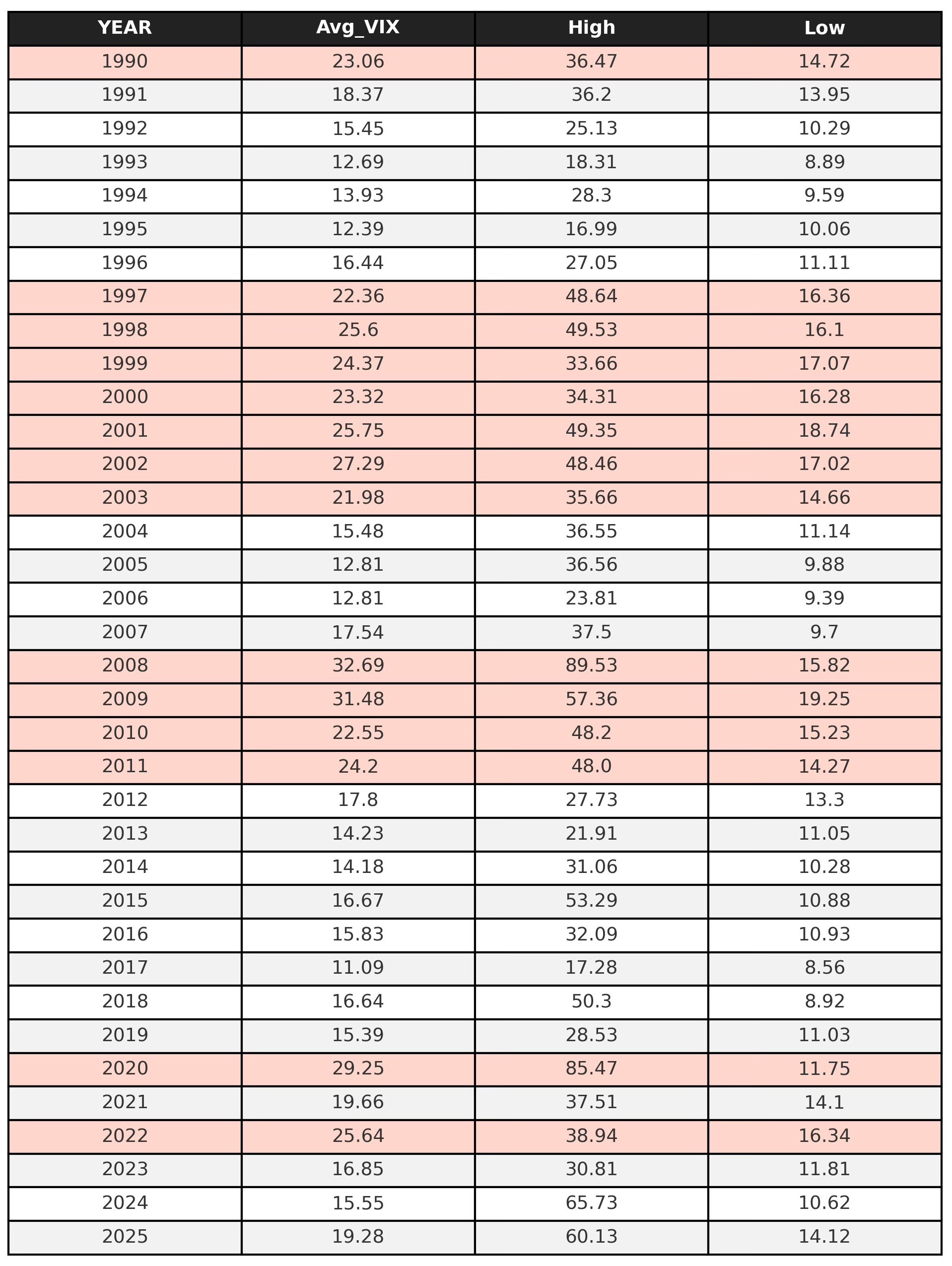

When you study 35 years of VIX data (from 1990 through 2025) you realize volatility tends to live in long-lasting “regimes.”

The results show multi-year periods where “normal” volatility levels vary from one regime to the next.

Each regime lasted 3 to 7 years on average, with clear breaks marked by macro or policy shocks.

Why Volatility Regimes Matter

Most Trading Strategies behave differently across different volatility clusters.

A system that performs well in low volatility environments often fail in high volatility environments and vice versa. That’s why in our backtests, we always bucket results by volatility regimes (low, medium, high).