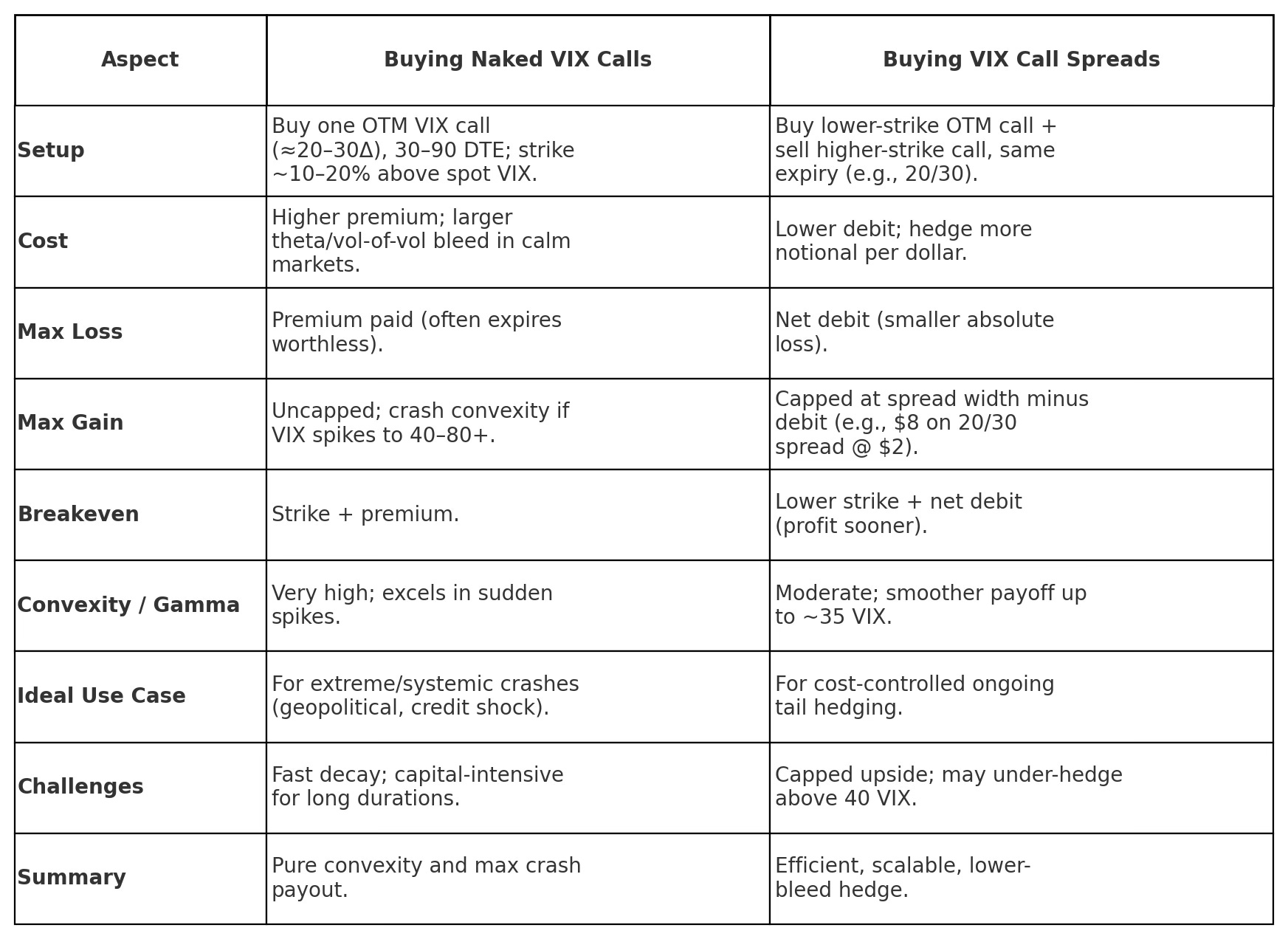

Is it Better to Buy Naked VIX Calls or Call Spreads?

Which is better for hedging against tail risk?

When stock markets crash, volatility can rise sharply. The VIX often doubles or even triples during crisis periods, offering one of the few instruments that move sharply against stock portfolios.

In March 2020, for example, the S&P 500 plunged –34% while the VIX spiked +260%. Such convex behavior makes VIX options a cornerstone of institutional tail-risk hedging.

Yet not all volatility hedges are created equal. Two popular approaches of buying naked VIX calls and buying VIX call spreads can both profit from volatility surges, but they differ drastically in cost, payoff shape, and portfolio efficiency. Understanding when to use each can determine whether your hedge cushions a drawdown or quietly bleeds capital.

Which Is Better?

For most investors, VIX call spreads deliver superior premium efficiency and scalability. They achieve roughly comparable protection at 40–60% lower cost, according to multiple backtests. Because most volatility hedges expire worthless, controlling bleed is essential for long-term portfolios.

However, naked VIX calls remain indispensable when your goal is unbounded convexity, the kind that transforms a 1% portfolio allocation into a double-digit gain during black-swan events.

Both naked VIX calls and call spreads hedge tail risk—but they serve different objectives.

Choose naked calls when you seek pure, explosive convexity against catastrophic events.

Choose call spreads for steady, budget-controlled insurance that cushions 10–20% equity drawdowns without destroying long-term returns.

The optimal solution lies in combining them: use call spreads for baseline protection and naked calls for the “doomsday” convex kicker.