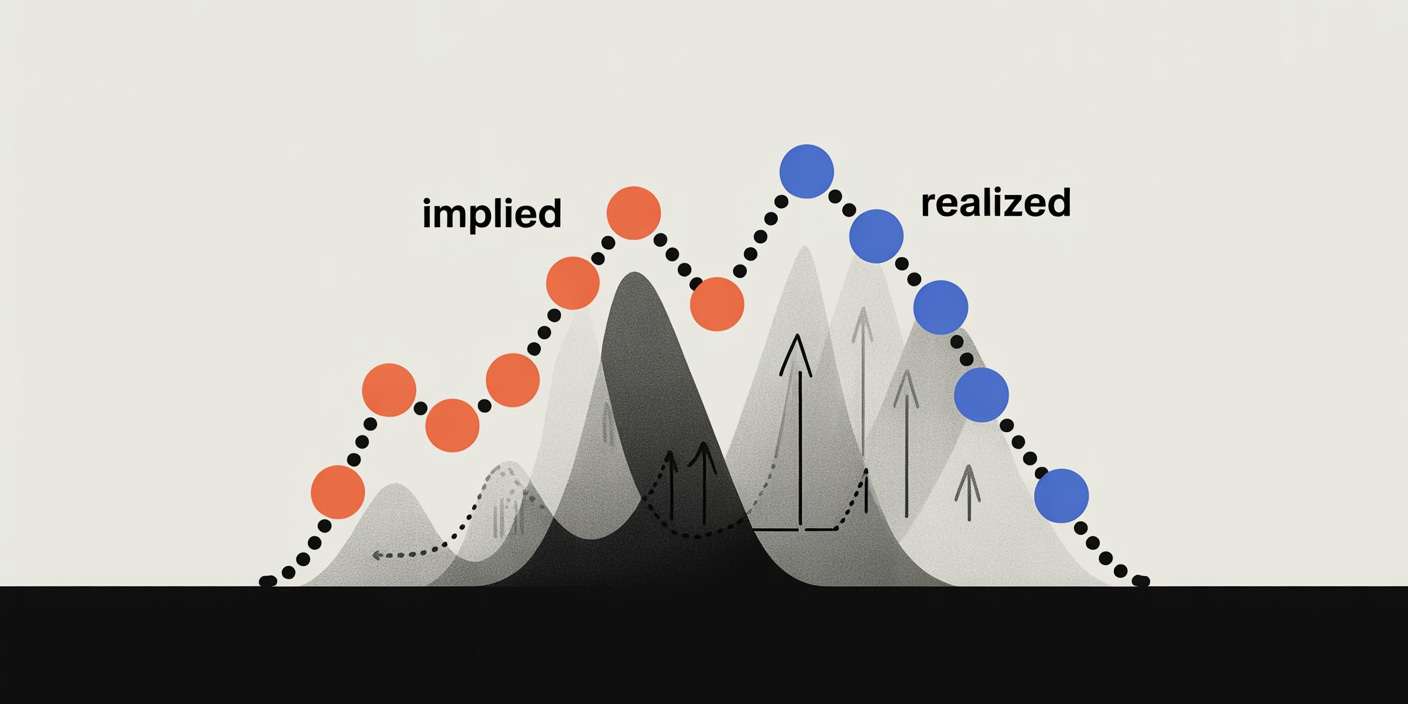

What Is Realized Volatility?

Realized volatility (RV) is a historical-looking measure. It tells you how volatile a stock has been in the past.

Calculated using historical price data (daily returns, intraday moves, etc.).

Expressed as an annualized percentage.

Example: If the S&P 500 moved 1% up and down daily over the past month, the realized volatility might be around 16% annualized.

RV is factual. It shows what has already happened.

What Is Implied Volatility?

Implied volatility (IV) is a future-looking measure. It reflects the market’s expectation of future volatility.

Higher option premiums = higher implied volatility.

Lower option premiums = lower implied volatility.

IV doesn’t tell you what will happen, it tells you what the market is pricing in.

Example: If traders expect big moves around an earnings release or a Federal Reserve decision, IV rises even before any move occurs.

Key Differences

Direction in Time

RV: Past movement (what happened).

IV: Future expectation (what might happen).

Source of Information

RV: Historical returns.

IV: Option market pricing.

Nature

RV: Objective, calculated directly from past price data.

IV: Subjective, depends on supply and demand in the options market.

How Traders Can Use This Information

The spread between implied volatility and realized volatility is at the heart of many strategies:

IV > RV: Options may be overpriced. Traders who sell options can benefit by collecting premium that exceeds actual realized moves.

IV < RV: Options may be underpriced. Buyers of options benefit because the market is underestimating actual movement.

This difference is sometimes called the volatility risk premium.

Sometimes, big opportunities lie in the gap between the two. For beginners, simply tracking IV and RV side by side can sharpen timing and improve strategy selection.