Beginner’s Guide to Price-Insensitive Flows

Price-insensitive flows are when stocks are bought regardless of price.

Imagine a buyer who must purchase a stock regardless of whether it’s trading at $50 or $150 per share.

This insensitivity to price pushes stocks higher.

Key Examples

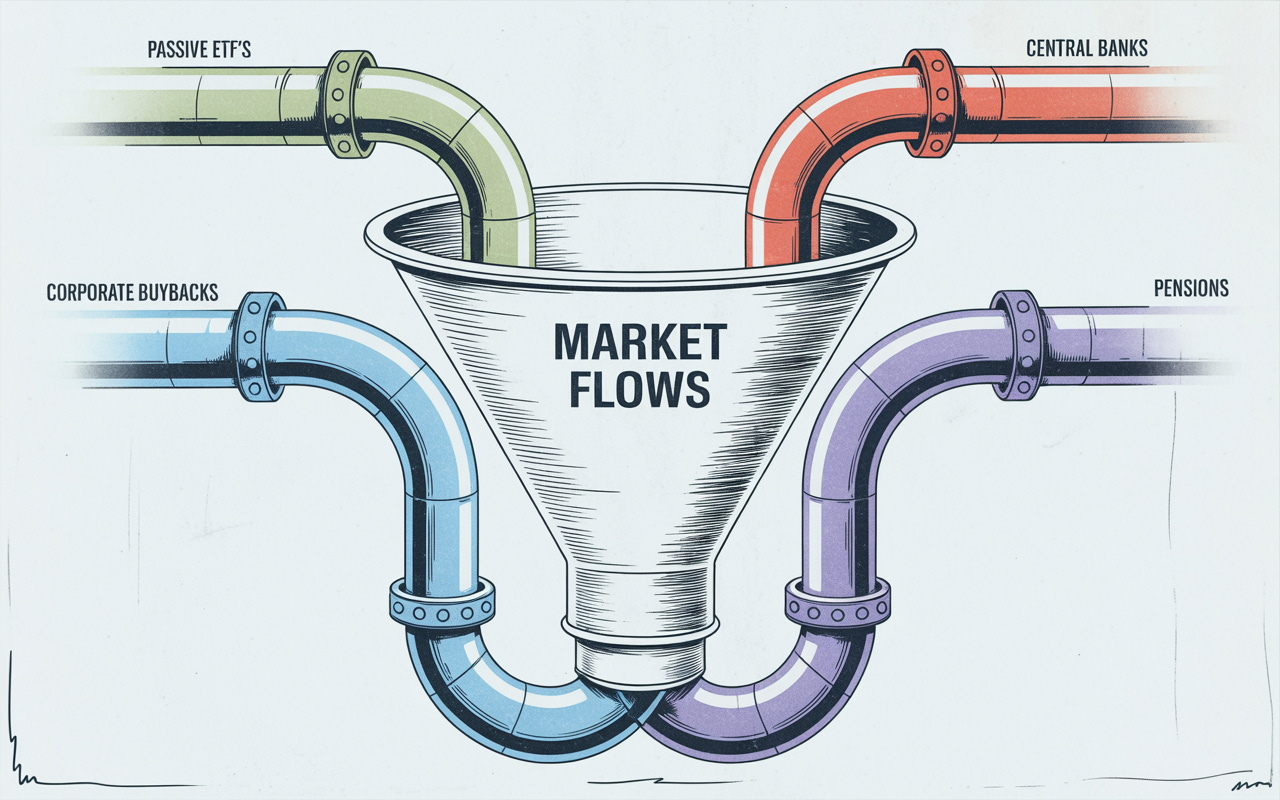

Price-insensitive flows come from various corners of the financial ecosystem. Here are some of the most prominent examples:

Corporate Share Buybacks: Companies repurchase their own stock using free cash flow or borrowed funds, often regardless of share price. They do this to return capital to shareholders and offset dilution from employee stock programs.

Many buybacks are executed by computers that buy a preset daily amount regardless of price.

Passive Investment Inflows: These flows are mostly from retirement accounts and other pension contributions. For example, when you put money in a 401(k), it buys shares of big companies (e.g., Apple or Nvidia) without caring if they’re expensive.

These happen on:

month-end

quarter-end

semi-annual windows

Again regardless of price.

Central Bank Interventions: Actions like quantitative easing (QE), where central banks purchase assets to inject liquidity, often ignore price levels.

How Price-Insensitive Flows Distort Market Valuations

These flows are pumping money into assets without scrutinizing whether they’re “cheap” or “expensive.” The result? Distorted valuations that can persist far longer than economic fundamentals might suggest, leading to bubbles, mispriced risks, and frustration for investors who rely on classic tools like the price-to-earnings (P/E) ratio.

Can They Reverse?

Reversals in price-insensitive flows almost always require a structural shock, not just a headline or a bad day in the markets. In short: these flows don’t reverse because “valuations are stretched”, they reverse when macro conditions force the flows to stop.